will the DXY test 120 again?

DXY WEEKLY CHART

The DXY is currently trading around 108. In the past it has traded as high as 160 and as low as 80. All big up movements in the DXY has been associated with some form of distress in the debt markets in the form of a financial crisis. We think that there is a good chance of the dollar testing 120 level from a technical point of view as the dollar has broken out of a multi month consolidation. Today we will look at some of the scenarios that might cause the DXY to go to 120 from a fundamental view.

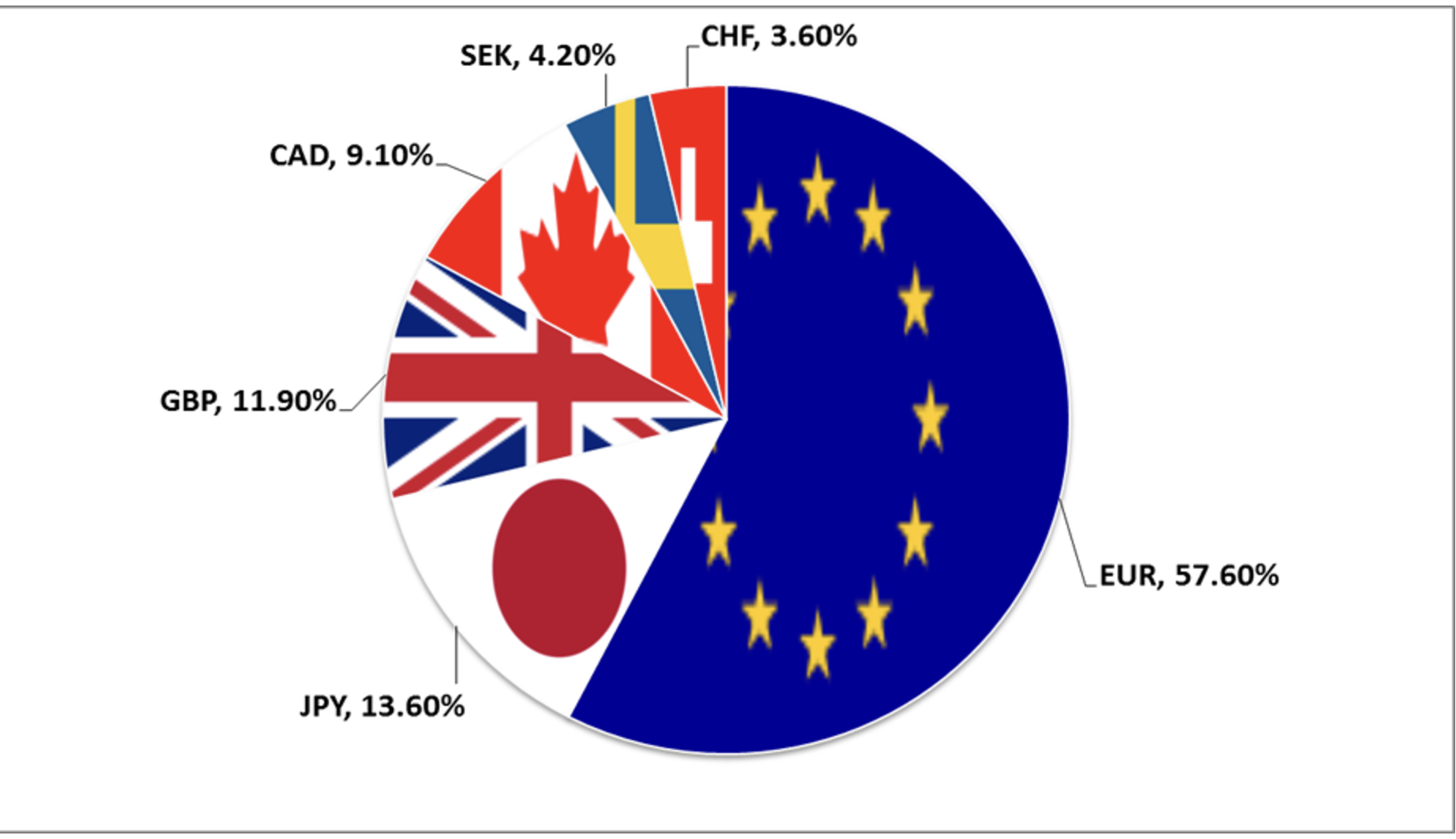

The US dollar basket

The slow death of the Euro:

The DXY is a measure of the dollar against a basket of currencies and Euro has the biggest weighting in this at around 60%. So for the dollar to go up by 15% Euro should fall by at least that much. There are plenty of reasons as to why the eurozone could collapse in the coming years.

Internal divisions and paralysis of the European parliament: The European parliament is complex and is composed of many centre wing parties and left parties but none of them have a clear majority in the parliament .So difficult decisions are unlikely to be passed in the parliament leading to paralysis. This is coming at an important time where there has been increasing geopolitical tensions and economic turbulence from the rise of Asia as a direct challenge to the western dominance. Also the eurozone contribution to the World’s GDP has been steadily falling over the years. So unless the current conditions change at the European parliament, it is unlikely that they will be able to enact difficult decisions to change the current path being taken

A detached European elite leading to political crisis: The European elites are completely detached from the views of the people of europe. They have encouraged more and more federalisation of Europe which is against the popular view. They have also encouraged uncontrolled immigration which is also against the popular view. This has led to the rise of the right wing parties in Europe. If the European elites continue their current policies, then these right wing parties will gain more seats in the parliament and can potentially become the ruling party in some countries. As the economic conditions deteriorate due to the ongoing war in Ukraine there may be a call to action to try and come out of the EU or to have better relationships with Russia to access cheap energy. This can lead to potential disintegration of the EU

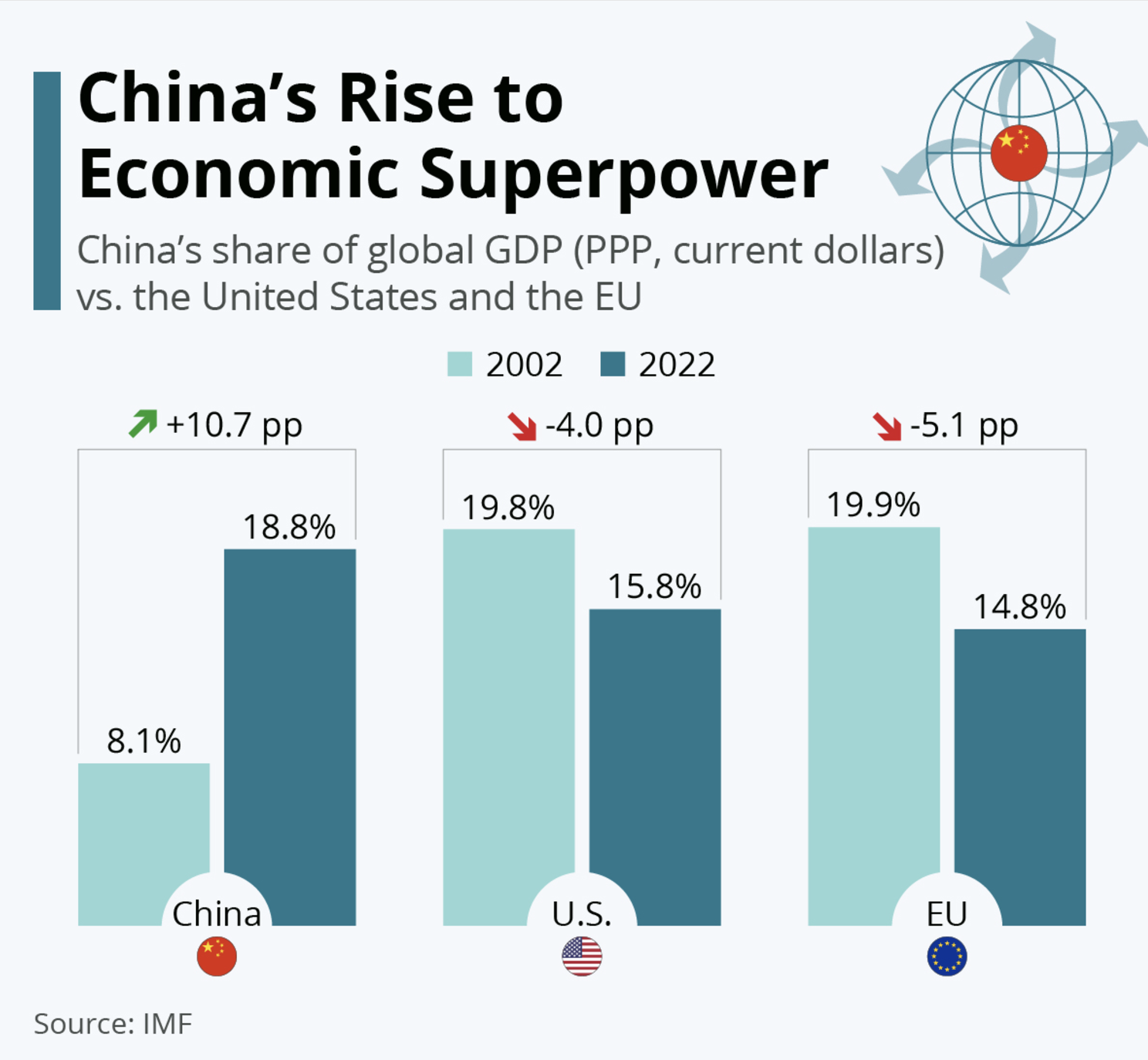

A Eurozone economic decline and debt crisis: The contribution of the Eurozone to the world GDP is steadily falling over time. If we look at the graph, we can see that this is mainly due to china gaining market share in sectors where Germany used to dominate. As China moves up the value chain the biggest losers will be high cost producers in Europe. Many countries in Europe have an ageing population and have a huge debt load and the current bureaucratic regulations make growth difficult within the Eurozone. So there is a good chance that we may see a crisis similar to the Greek financial crisis. During the Greek financial crisis, the German and French banks were bailed out. But if bigger economics like France or Italy have problems, then the ECB might lose control of the bond market. This can cause economic chaos and result in the slow disintegration of the Eurozone.

Oil and Geopolitics: Having weaned itself from Russian energy, the EU is heavily dependent on LNG supplies from the US and the Middle east. The middle east is becoming increasingly unstable and any disruption in the sea routes where the energy passess will severely impact energy supplies to the EU and cause a spike in energy prices. This will have an effect on eurozone inflation and also the collapse of European industry. The Dollar will benefit from high oil prices as the US is the biggest producer of oil and Trump will relax drilling regulations and this will cause an increase in oil production at least in the near term. Another overlooked concern is political instability in Iran and Saudi Arabia as both are big exporters of Energy

Tariffs and economic wars: If tariffs are introduced and counter tariffs imposed, Europe will find it very hard to be competitive outside of itself. They really can not produce any goods cheaper than China and now with increased energy costs and tariffs, they won't be able to compete with manufacturers in the EU. This economic stagnation will cause debt to GDP levels of eurozone countries to rise and put increasing pressure on the EU. The EU might be forced to do yield curve control

China’s rise as an economic superpower has come from declines in GDP output from both USA and Eurozone and more so from Eurozone. The current high energy costs due to loss of cheap Russian gas, high labour costs and EU bureaucracy. The captive market means there is no competition and this reduces their global competitiveness and innovation. This is why we favour the US over the EU.

The Pound:

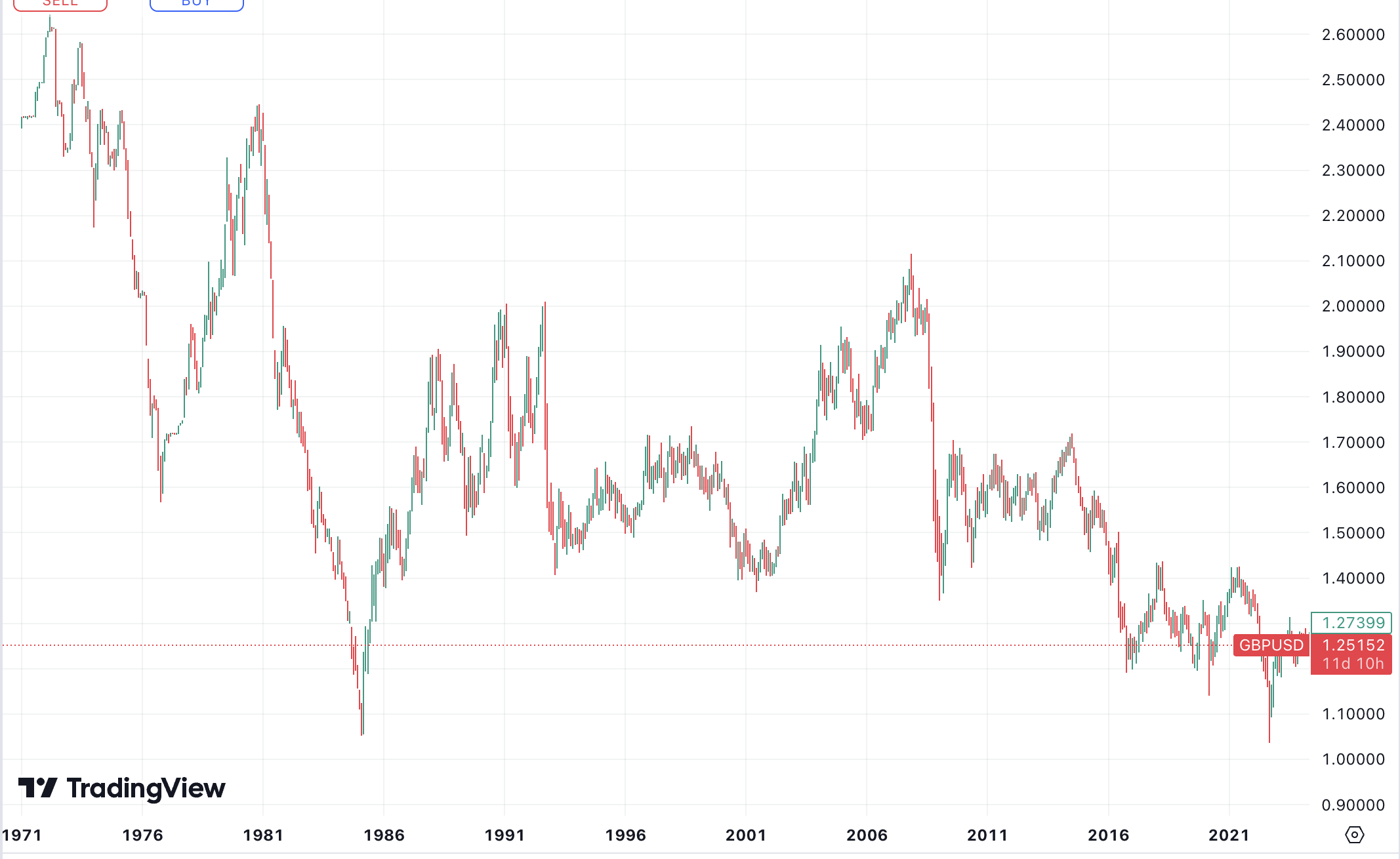

The British pound contribution to the DXY basket is about 11%. Even though the UK has exited from the EU, the majority of its trade is still with the EU and will be affected with problems in the Eurozone. Several decades of being within the Eurozone has made British industry less innovative and competitive. The UK also has some of the highest energy costs and labour costs in the west. Although they may no longer be bound by the EU laws, they are still forced to follow many laws of the EU inorder to be able to trade with the EU. This will make it less competitive in the world.

GBPUSD monthly chart

We can see that the pound has been in gradual decline since 1970’s with its value falling by 50%. If we chart the pound vs the Swiss Franc, this will be even worse. The UK’s used to be one of the important financial centre after New York. However since the financial crisis of 2008, increasing regulation meant that the UK is slowly losing ground in one of its biggest revenue earner. Other centres like singapore and Dubai are taking some of the business away from UK. Also it will take time for UK to readjust to the changing world order. But it is in a better position than EU in this regard.

The Yen:

We don't need to elaborate on the problems of the Yen. They have the highest debt and the currency has already depreciated by more than 50% in the last 2 years . They do have certain advantages in the form of having nearly a trillion dollars in US treasuries which they can repatriate at twice the value due the fall in Yen. They will continue to keep the yields below the inflation rate as a means of financial repression. As a means to avoid the financial repression, we hypothesize that a lot of private money has left Japan and in invested in US equities and real estate. If we have significant falls in the equity markets, then this money is likely to be repatriated back and this might cause Yen to rise just like we saw during the 2008 financial crisis.

USDJPY monthly chart- There has been a 100% depreciation in the Japanes Yen since 2012.

Japan is dependent on energy imports and any rise in the costs of these will be bad for the currency. They however are in proximity to rapidly growing south east asian economies and they could benefit from increased trade from these countries.

Nobody can predict the future accurately. We can only take educated guesses on possible outcomes. There are so many variables there is potential for these variables to change and result in different outcomes. The strategist should take into account these changing variable and be flexible to these changes. In our view, the DXY will continue to drift higher unless there is a significant change in the current variables. The value of the Dollar in terms of real assets like real estate, gold and equities will fall even as the dollar index rises to 115 first and then to 120. Geopolitical escalation and a financial crisis will accelerate these outcomes.